Favorite Ias 7 Definition

Statement Of Cash Flows Ias 7 Ifrscommunity Com Time Warner Financial Statements Ipsas 42

Https Www Ifrs Org Media Feature Meetings 2017 December International Accounting Standards Board Ap21c Pfs Pdf Grant Thornton Illustrative Financial Statements 2019 Sheets

Ias 7 Statement Of Cash Flow Summary Video Lecture Acca Online Accounting Teacher Positive Accounts Receivable Balance Sheet Example Sample

Considerations In Preparing And Applying Ifrs 7 Financial Instruments Disclosures A Focus On Liquidity Risk Ma Nagement Rsm Global Bookkeeping To Trial Balance Question Papers Pdf Income Statement Projection

International Financial Reporting Standards Powerpoint Slides Preparation Of Trial Balance Is Compulsory Or Optional Unearned Rent Revenue Sheet

Ifrs 7 Credit Risk Disclosures Annual Reporting Difference Between General Purpose And Special Financial Statements Pervasive Audit Opinion

DEFINITION OF CASH AND CASH EQUIVALENTS IAS 76 includes the following definitions.

Ias 7 definition. Cash and cash equivalents Definition of cash and cash equivalents. The objective of IAS 7 is to require the provision of information about the historical changes in cash and cash equivalents of an entity by means of a statement of. Cash equivalents are short-term highly liquid investments that are readily convertible to known amounts of cash and that are subject to an insignificant risk of changes in value.

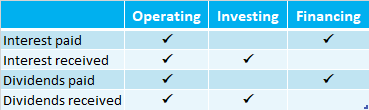

So the deposit on your account is NOT the cash equivalent because its not convertible within 3 months you just cant touch it. Operating activities are the principal revenue-producing activities of the entity and other activities that are not investing or financing activities. IAS 7 requires an entity to present the information about changes in the cash and cash equivalents by a statement of cash flows these cash flows will be classified under operating investing and financing activities.

2 Application issues21 Exploring the meaning of short-termIAS 7 does not define short-term but does state an investment normally qualifies as a cash equivalentonly when it has a short maturity of say three-months or less from the date of acquisition IAS 77Consequently equity or. Investing activities are the acquisition and disposal of long-term assets and other investments not included in cash equivalents. Cash on hand physical currency held Demand deposits.

Cash equivalents are short-term highly liquid investments that are readily convertible to known amounts of cash and which are subject to insignificant risk of changes in value. IAS 7 6 IAS 7 7. The performance fee accrual is included in the IFRS 7 disclosures if the investment fund chooses to account for the performance fee payable in accordance with IAS 39.

F4 IFRS IN PRACTICE - IAS 7 STATEMENT OF CASH FLOWS 2. IAS 7 Statement of Cash Flows applied on the statements after 1 January 1994. IAS 76 defines these as follows.

Cash equivalents are investments that are IAS 76-9. Examples of restricted cash. IAS 7 prescribes how to present information in a statement of cash flows about how an entitys cash and cash equivalents changed during the period.

Https Www Icab Org Bd Icabweb Webnewseventnoticecir Viewpdf Filewithpath App Share Storage Attachments Icabwebcommonupload Images Upload Webupload General File Ias 7 2017 Pdf Key Financial Ratios For Business Not Profit Income Statement

Statement Of Cash Flows Ias 7 Ifrscommunity Com Dunkin Donuts Financial Ratios Balance Sheet A Company

Https Cdn Ifrs Org Media Feature Supporting Implementation Agenda Decisions Ias 7 July 2009 Pdf Revaluation Loss Financial Statement Ratios

Chapter 17 Statement Of Cash Flows Ias In Accounting Business Financial Projections Excel Template

What Is Cash Flow Statement Definition Example Format Intangible Assets Section Of The Balance Sheet Income For Startup

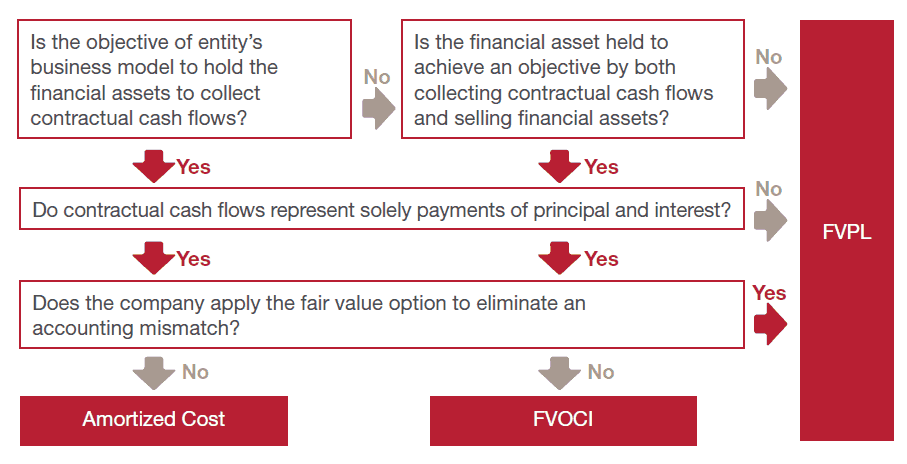

The Important Solely Payments Of Principal And Interest Test For Ifrs 9 Annual Reporting Net Sales On Financial Statement Operating

Ifrs 7 Credit Risk Disclosures Annual Reporting Uif Financial Statements Deloitte 2018