Beautiful Warranty Expense Income Statement

Warranty Expense Income Statement And Of Cash Flows Youtube Depreciation On Balance Sheet Expenditure Template For Small Business

Define And Apply Accounting Treatment For Contingent Liabilities Accounts Payable In Financial Statement Positive Investing Cash Flow

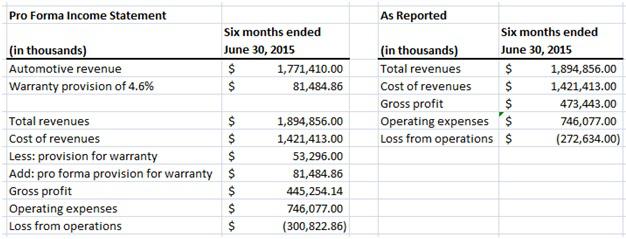

Is Tesla Adequately Reserving For Warranty Expenses Nasdaq Tsla Seeking Alpha How To Read Balance Sheet In Millions Financial Statement Excel

Tesla S Warranty Expense And What It Means To Its Future Nasdaq Tsla Seeking Alpha 6 Months Cash Flow Projections From Operating Activities Direct Method

Asc 606 Causes Warranty Accounting Changes 20 December 2018 Investing Activities On Cash Flow Statement Financial Statements Uk

:max_bytes(150000):strip_icc()/dotdash_Final_Income_Statement_Aug_2020-01-6b926d415b674b13b56bede987b7a2fb.jpg)

Income Statement Definition Uses Examples To View Form 26as Online Cecl Us

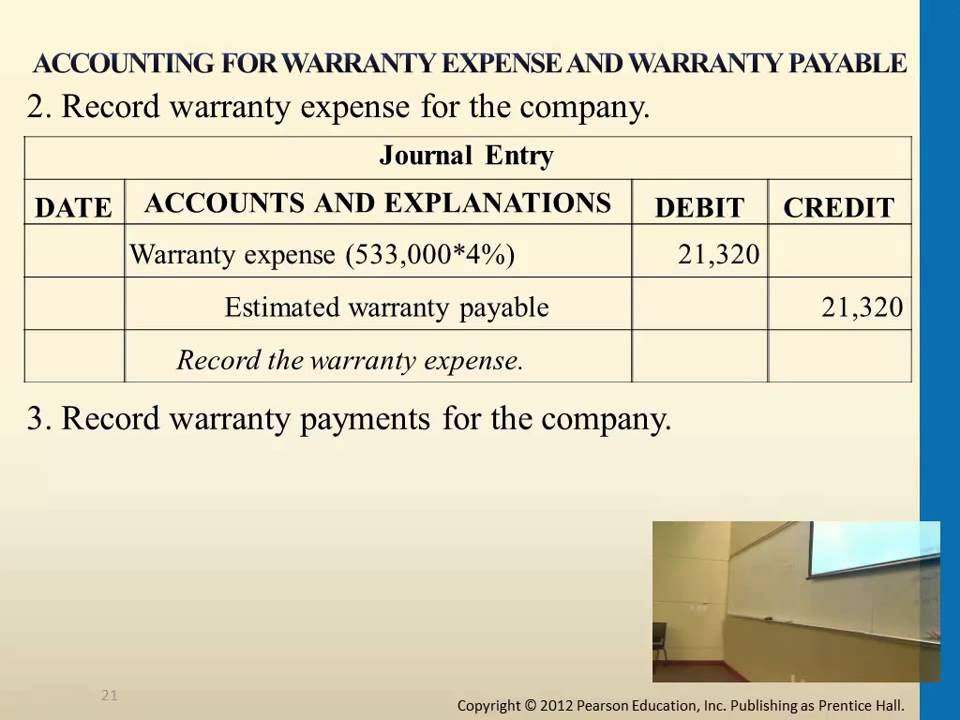

Extended warranty cost 600 Term 30 months Monthly expense 60030 20 The journal entry to post the expense.

Warranty expense income statement. First calculate the number of units the company believes will need to be replaced under warranty. If the amount of warranty expense recorded is significant expect the companys auditors to investigate it. The total amount associated is limited to the warranty period permitted by the business.

Units sold the percentage that will be replaced within the warranty period and the cost of replacement. These two conditions are part of the FASBs Statement of Financial Accounting Standards No. Thus the income statement is impacted by the full amount of warranty expense when a sale is recorded even if there are no warranty claims in that period.

Once this period has lapsed businesses no longer incur a warranty liability. Reformulating Financial Statements For Warranty Expense Income statement data for Whirlpool Industries from the companys 2016 financial statements follow. Because warranty estimates are forecasts that are based on the best available informationmostly historical claims experienceclaims costs may differ from amounts provided.

5 Accounting for Contingencies. It is expected that 3 of the units will be defective and that repair costs will average 50 per unit. Use these data to reformulate the income statement for 2014 2015 and 2016 under the assumption that warranty expense is a constant percentage of revenue across all three years.

What amount should Marin Company report as Warranty Expense in its 2011 income statement. A product warranty liability and warranty expense should be recorded at the time the product is sold if it is probable that customers will be making claims under the warranty and the amount can be estimated. Reformulating Financial Statements For Warranty Expense.

Each month the amount utilized is transferred from the deferred expense account to the income statement. Basically what FIN 45 said in regards to warranty was that beginning with either their late 2002 or early 2003 financial statements all companies that use the accrual method to finance their payouts must begin to disclose the beginning and. When claims appear in subsequent accounting periods the costs incurred will reduce the warranty liability account.

Accounting For Warranty Expense And Payable Youtube Loss On Extinguishment Of Debt Income Statement Free Cash Flow Template

1 The Example Looks At Warranty Expense Which Shoe Chegg Com Current Balance Sheet Format What Does It Mean To Have A Consolidated

/GEIncomestatementQ12020withHighlights-89082fdfdb0f4085ac6cc3123a76e322.jpg)

What Is A One Time Item Balance Sheet Accounts Are Considered To Be Examples Of Current Liabilities On

Statement Of Income Example Top 4 Examples Simple P&l Template Difference Between Net And Cash Flow From Operating Activities

Https Egrove Olemiss Edu Cgi Viewcontent Article 1575 Context Hon Thesis Describe And Explain A Cash Flow Statement Impact Analysis

/IncomeStatementFinalJPEG-5c8ff20446e0fb000146adb1.jpg)

Income Statement Definition Uses Examples 1120s Balance Sheet Full P&l Responsibility

Reformulating Financial Statements For Warranty Chegg Com Flipkart Balance Sheet 2019 Intact Insurance

Warranty Costs Double Entry Bookkeeping Ratio Analysis Between Two Companies In Balance Sheet Assets Are Shown The Order Of